The era of easy capital and unchecked proliferation of technology startups has officially given way to a rigorous market correction, according to a new report released by Silicon Valley Bank (SVB). Analyzing the trajectory of venture-backed companies from the peak of the pandemic boom in 2022 through early 2026, the data paints a stark picture of an ecosystem in contraction. For founders, investors, and industry observers, this report serves as a definitive signal that the "growth at all costs" mindset has been replaced by a survival-of-the-fittest landscape where capital efficiency is the primary currency.

This analysis is particularly crucial for entrepreneurs currently seeking funding or navigating the "Series A crunch." The data suggests that the reduction in active startups is not merely a pause but a structural reset. While the total number of funded entities has decreased, the concentration of talent and capital is shifting back toward established hubs, challenging the narrative of the "rise of the rest" that dominated the last decade. Understanding these regional and macro trends is essential for strategic planning in the current fiscal year.

The End of the ZIRP Era and Startup Attrition

The primary driver behind the trends identified in the SVB report is the delayed but profound impact of ending the Zero Interest Rate Policy (ZIRP). During the 2020-2021 boom, venture capital flowed freely into non-traditional tech hubs and speculative business models. However, the data since 2022 reveals a significant "thinning of the herd." As interest rates rose and limited partner (LP) liquidity tightened, the bar for follow-on funding raised dramatically. Consequently, companies that could not demonstrate a clear path to profitability have exited the ecosystem via dissolution or distressed asset sales.

This attrition rate is not uniform across all sectors. While deep tech and AI-focused enterprises continue to attract significant capital, SaaS and consumer tech startups have faced the brunt of this contraction. The report indicates that the "mass extinction" event predicted by many VCs in 2023 has largely played out, leaving a smaller, leaner, but potentially more robust cohort of companies remaining in the market. This consolidation suggests that while there are fewer startups today than in 2022, the average quality and resilience of the surviving entities are likely higher.

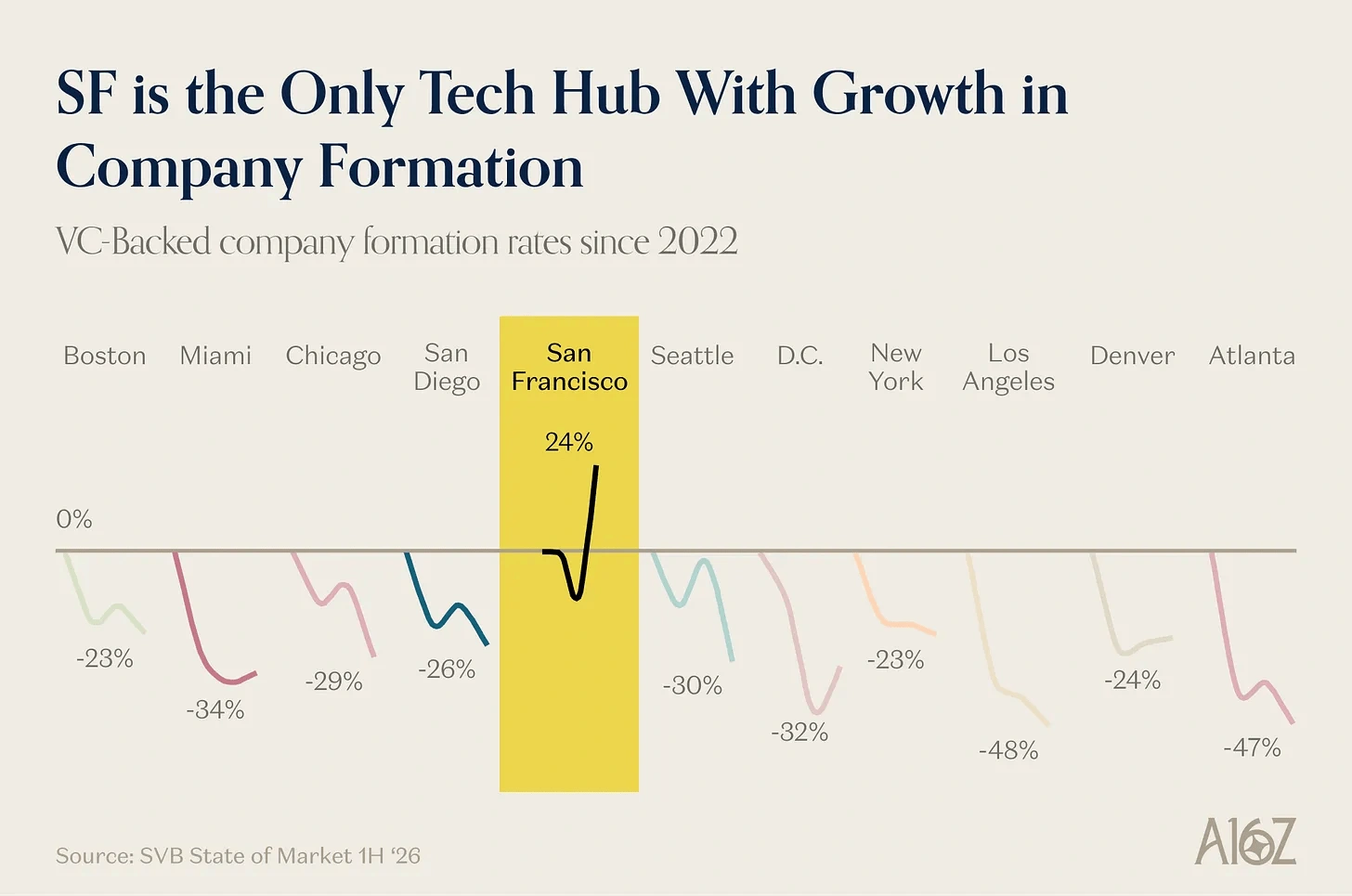

Regional Analysis: The Resilience of the Bay Area

One of the most compelling aspects of the SVB data is the geographic breakdown of startup activity. Contrary to the popular "exodus" narrative, the San Francisco Bay Area has demonstrated remarkable resilience relative to emerging hubs. While the total number of startups has declined nationally, the percentage drop in established hubs like Silicon Valley and Boston has been less severe compared to pandemic-era boomtowns like Austin and Miami.

The data suggests a "flight to quality" not just in assets, but in geography. When capital becomes scarce, investors retreat to ecosystems with the deepest networks of talent, experienced mentors, and acquisition opportunities. Emerging hubs, which saw explosive growth when capital was abundant, are now seeing a sharper correction as the remote-work arbitrage normalizes and the necessity of physical proximity for deep-tech collaboration (especially in AI hardware and biotech) reasserts itself.

| Metro Region | Trend Since 2022 | Key Driver |

|---|---|---|

| San Francisco Bay Area | Moderate Contraction | High retention due to AI boom and talent density. |

| New York City | Stable / Slight Decline | FinTech and Enterprise resilience anchored the market. |

| Austin & Miami | Significant Decline | Correction of pandemic-era hype; retreat of tourist capital. |

| Boston | Stable | Biotech and Robotics sectors require long-term, sticky capital. |

Strategic Implications for Founders in 2026

For founders operating in this constrained environment, the message is clear: metrics matter more than vision. The SVB report implicitly advises that the days of raising rounds on pure potential are over. Startups must now operate with the discipline of public companies from a much earlier stage. This means maintaining a longer runway, prioritizing unit economics over top-line growth, and understanding that the next funding round is far from guaranteed.

Furthermore, the regional data suggests that location strategy should be revisited. While remote work remains a feature of the modern workplace, the concentration of capital in Tier 1 hubs implies that founders in secondary markets may need to work twice as hard to secure face time with top-tier VCs. Building a network in these core hubs, even if the company is headquartered elsewhere, is becoming a critical component of fundraising strategy.

Frequently Asked Questions

- Why has the number of VC-backed startups declined since 2022?

The decline is primarily due to higher interest rates, reduced VC liquidity, and a market correction that eliminated companies lacking sustainable business models (the end of the ZIRP era). - Which US regions are holding up best in the current startup climate?

Established hubs like the San Francisco Bay Area and New York have shown more resilience compared to pandemic-boom cities like Austin and Miami, largely due to the AI boom and deep talent pools. - Is Venture Capital funding drying up completely?

No, funding is not drying up, but it is becoming highly concentrated. Capital is flowing heavily into high-conviction sectors like Artificial Intelligence and Defense Tech, while general software startups face higher scrutiny.

My Take

The SVB report confirms what many in the industry have felt anecdotally: the party is over, but the work has just begun. This contraction, while painful, is ultimately healthy for the technology sector. It flushes out noise and refocuses resources on genuine innovation rather than arbitrage. For investors, 2026 represents a vintage year opportunity where valuations are rational and founders are disciplined. For entrepreneurs, the challenge is immense, but those who survive this cycle will likely build the defining companies of the next decade.