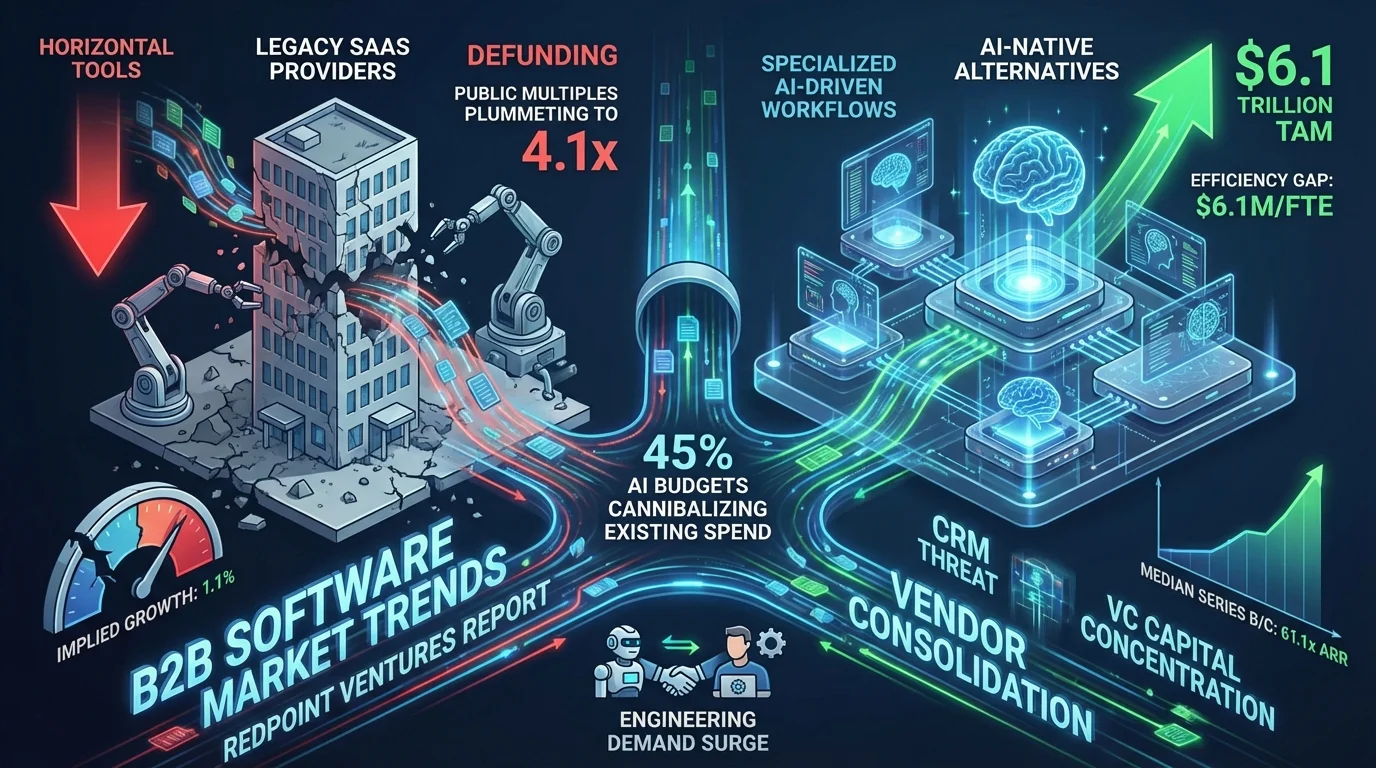

The B2B software market trends for 2026 reveal a brutal reality for legacy SaaS providers, as enterprise buyers aggressively defund traditional platforms to finance AI-native alternatives. A new 70-slide market update from Redpoint Ventures, surveying 141 CIOs, exposes a massive shift where 45% of artificial intelligence budgets are directly cannibalizing existing software spend. For enterprise founders and IT executives, this data dictates an immediate strategic pivot away from seat-based horizontal tools toward highly specialized, AI-driven workflows.

The financial markets are already pricing in this disruption, with public SaaS multiples plummeting to 4.1x next-twelve-months (NTM) revenue, marking the lowest point since 2008. Investors have slashed implied long-term growth rates from 4.7% to just 1.1%, signaling a belief that AI will permanently compress traditional software moats. Consequently, software stocks have dropped 20% year-to-date, drastically underperforming sectors like Energy, which is up 32%, and broader IT, which is down only 11%.

The bleeding is heavily concentrated in horizontal SaaS, which has plummeted 35% over the last twelve months. In contrast, vertical SaaS is up 3%, and infrastructure has gained 2%. This divergence indicates that tools built to serve every industry equally are the most exposed to AI automation, while deeply integrated, industry-specific platforms retain their defensive moats.

The CRM Threat and Vendor Consolidation

Enterprise buyers are actively shrinking their software stacks, with 54% of surveyed CIOs pursuing vendor consolidation. Furthermore, 58% of IT leaders identify AI feature additions as the primary driver of increased software spending. Because only 3% of CIOs expect AI to increase their total number of vendors, net-new recurring revenue acquisition has become a zero-sum game for incumbents.

Customer Relationship Management (CRM) is currently the most vulnerable category in the enterprise stack. A staggering 83% of CIOs are open to replacing their Salesforce Automation tools with an AI-native vendor. Other highly contested areas include customer service management at 56%, ITSM at 55%, and ERP and procurement tied at 50%. Conversely, deeply embedded technical workflows like finance operations (14%), DevOps (19%), and project management (19%) remain highly resistant to rapid replacement.

The AI-Native Efficiency Gap

A massive structural divide has emerged in revenue generation per full-time employee (FTE) between legacy software and AI-native startups. Company Cursor currently generates an astonishing $6.1 million per FTE, followed by startup Lovable at $3.4 million, OpenAI at $1.5 million, and Anthropic at $1.2 million. This completely eclipses traditional giants like platform Salesforce ($0.54 million), Datadog ($0.51 million), ServiceNow ($0.49 million), and Atlassian ($0.46 million).

This 12x efficiency gap between company Cursor and platform Salesforce is driving extreme private market valuations. Median Series B and C ARR multiples in 2026 sit at 61.1x, representing a 528% premium over public high-growth software, which trades at 9.7x. However, private AI companies are growing at a median rate of 640% year-over-year compared to 29% for public counterparts, justifying the massive capital influx.

Market Expansion and VC Concentration

To capture the remaining data points from the Redpoint Ventures report, the following metrics highlight the accelerated pace and expanding scale of the AI application layer:

- Accelerated Valuations: The time required to reach a $50 billion valuation has compressed from 23 years (pre-2000s) to just 9 years for the post-2000s cohort. Specifically, company Anthropic and company Cursor reached this milestone in 4 years, while startup xAI achieved it in just 1 year.

- A $6.1 Trillion TAM: The total addressable market expands massively as AI moves from copilots to task agents, workflow agents, and fully autonomous systems. While US software spend is $0.5 trillion, adding knowledge worker payroll pushes the potential TAM beyond $6.1 trillion.

- VC Capital Concentration: A massive 44% of all enterprise software venture capital dollars are now concentrated in the top 20 deals, up from 8% in 2020. Companies OpenAI, Anthropic, and xAI have dominated the top 5 deals consecutively across 2023, 2024, and 2025.

- Engineering Demand Surge: Contrary to job loss fears, AI is creating more demand for developers. Indeed job postings for software engineers have recovered to an index of 97, mirroring the 1973 introduction of ATMs, which ultimately expanded bank teller employment by 81% due to lowered operational costs.

My Take: The Death of the Traditional SaaS Model

The data from Redpoint Ventures confirms that the 2026 to 2027 window is an extinction-level event for horizontal, seat-based SaaS companies. When 45% of enterprise AI budgets are funded by canceling existing software contracts, incumbents can no longer rely on passive renewals. The staggering $6.1 million revenue-per-employee metric from company Cursor proves that the traditional B2B playbook - scaling massive sales and engineering teams to support bloated platforms - is structurally obsolete.

Furthermore, the extreme concentration of venture capital into foundation models like company OpenAI and startup xAI means application-layer founders must rethink their survival strategies. Being the second-best tool in a horizontal category is no longer fundable. Startups must pivot toward vertical software, embedding themselves into proprietary, industry-specific workflows where AI drives increased compute consumption rather than simply displacing human seats.