Legacy payment systems are quietly draining the competitive lifeblood of traditional banks, leaving them highly vulnerable to agile fintech rivals. As digital-focused firms rapidly deploy embedded finance and real-time payment networks, institutions clinging to outdated infrastructure risk losing their customer base before they even notice the shift. According to industry experts, falling behind in payment technology does not just limit current product offerings; it fundamentally cripples a bank's ability to respond to future financial innovations.

The technological gap is widening as the payments industry embraces new forms of automation and digital asset platforms. Andy Schmidt, global banking lead at CGI, notes that modernizing requires a multifaceted approach, including the adoption of real-time data architecture and modular, API-first frameworks. Furthermore, banks must integrate ISO 20022 structured data standards and apply artificial intelligence to their payment operations. Midsize and smaller institutions are struggling the most with these transitions, often misallocating their budgets toward maintaining legacy systems rather than funding necessary replacements.

This inertia carries a steep cost, particularly as instant payments and e-money wallets capture a larger share of the market. A recent report from Capgemini revealed that these digital methods accounted for 25% of global transaction volume in 2024, with projections reaching 32% by 2029. While some traditional institutions like U.S. Bank are successfully utilizing The Clearing House's Real-Time Payment network to instantly deliver funds to over 6,000 auto and RV dealers, the broader market remains heavily dominated by fintechs. Companies such as Dealer Pay, REPAY, and PayJunction are aggressively capturing niche markets like buy now/pay later (BNPL), consumer loans, and auto dealerships.

Strategic Roadmap: 7 Steps to Bank Payment Modernization

To survive the fintech encroachment, banks must overhaul their approach to payment infrastructure. Based on insights from industry leaders at Capgemini, Payforge, and Form3, institutions should follow this actionable framework:

- Think big picture: Abandon single-minded, one-off technology upgrades. Banks must define a holistic strategy that aligns payment architecture improvements with long-term revenue generation.

- Take an inventory: Map every existing integration, vendor dependency, and technical workaround. Understanding the baseline is critical, especially since many banks have lost institutional knowledge through outsourcing.

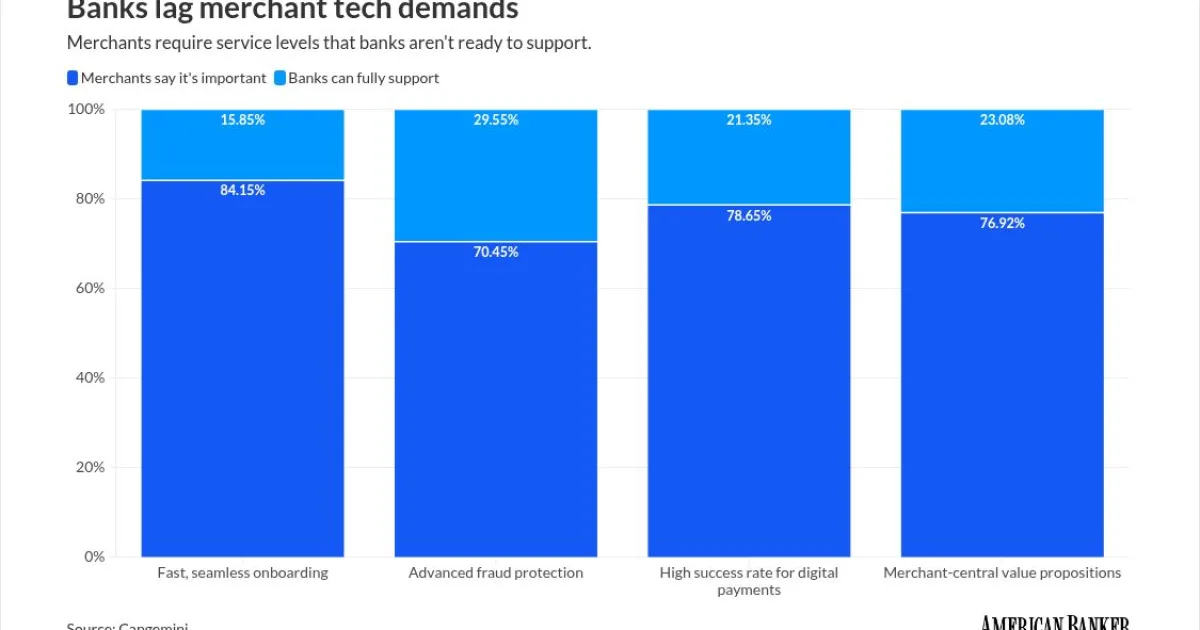

- Allocate resources appropriately: Shift financial resources away from the expensive maintenance of legacy systems and direct those funds toward building or acquiring modern replacement platforms.

- Focus on real-time payments: Prioritize the adoption of instant payment networks. Offering full real-time capabilities to both retail and business clients is essential to prevent competitors from stealing market share.

- Think futuristically: Do not wait for explicit client demand before innovating. Anticipate emerging use cases in sectors like BNPL, online gambling, and auto sales where fintechs are currently thriving.

- Follow the leaders: Emulate successful models like Cross River Bank, which built an in-house API-driven core to power embedded payments. By adopting RTP, FedNow, and partnering with companies like Plaid, they now move over $1 billion monthly in real-time disbursements.

- Consider a sidecar approach: If retrofitting old tech is too complex, launch a separate startup to experiment with new technologies. A prime example is NatWest Group, which built the digital bank account Mettle on entirely separate systems to serve small businesses.

My Take: The Fatal Flaw of Waiting for Demand

The most alarming revelation from this industry shift is the admission by Form3's Dave Scola that banks are delaying modernization simply because they do not see immediate client demand. In the technology sector, waiting for the customer to ask for a faster, more seamless experience is a fatal strategic error. By the time a retail customer or small business explicitly demands real-time API integrations, they have already opened an account with a fintech provider that offers it by default.

The "sidecar approach" utilized by NatWest Group to launch Mettle is arguably the most viable lifeline for midsize banks paralyzed by technical debt. Attempting to hot-swap a legacy core banking system is akin to changing the engine on a commercial jet mid-flight. By spinning up an independent, cloud-native entity, banks can immediately begin capturing the projected 32% global transaction volume of instant payments without risking their legacy operations.

Ultimately, the transition to real-time, API-driven payments is no longer a premium feature; it is the baseline infrastructure of modern commerce. Banks that continue to pour their IT budgets into patching outdated mainframes are merely funding their own obsolescence. The blueprint provided by Cross River Bank proves that early adoption of networks like FedNow and RTP is the only guaranteed mechanism for long-term survival.